Regulatory actuarial studies and IFRS

Actuarial studies under international and local standards

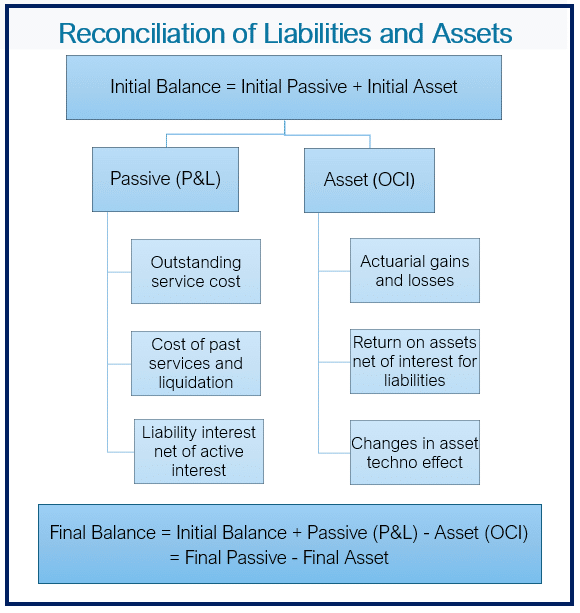

International Financial Reporting Standards (IFRS) require measurements using actuarial techniques, such as IAS 37, IAS 19, IAS 26 and IFRS 17. In addition, there are other accounting standards such as USGAAP, IPSAS and IFRS for SMEs that also require actuarial estimates for accounting purposes.

Actuarial advice on the adoption of international financial reporting standards and implementation of new standards

When adopting IFRS, companies must carry out a diagnostic process for the application of the new standards, as well as determining possible accounting adjustments. To carry out the implementation of standards that include actuarial measurements, the support of actuarial experts is required.

Actuarial guidance on regulatory standards

Each country in the Region has specific legislation for regulated entities that in some cases requires the preparation of actuarial analyzes and estimates based on the criteria given by local regulators.